SUMMARY

Measures taken so far by RBI have failed to woo the NBFC community, particularly in the digital domain

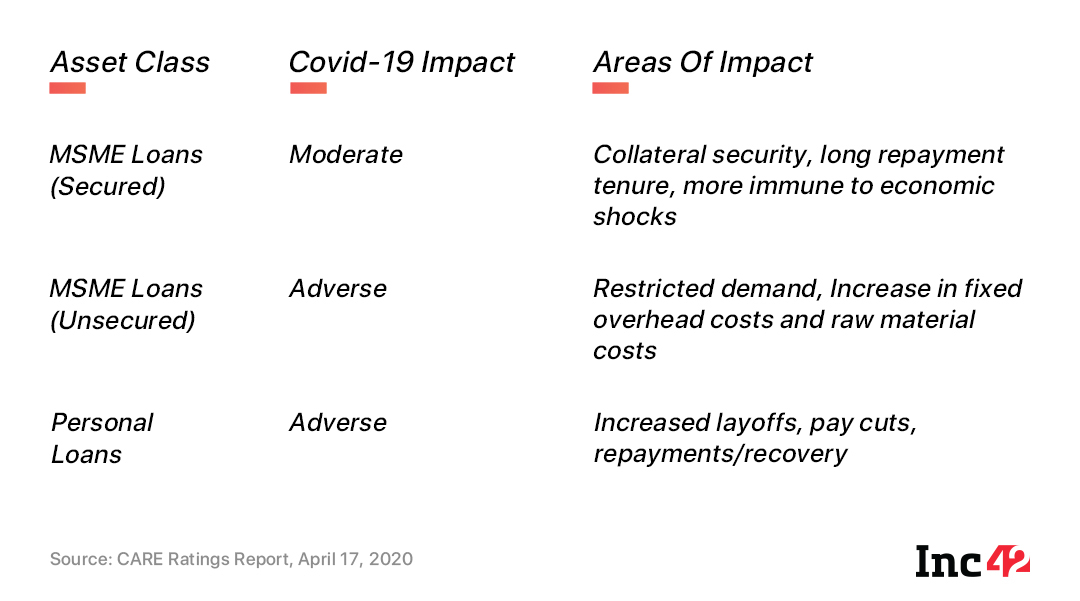

SME lending and consumer lending have both been severely impacted by the pandemic crisis

On May 4, RBI held a meeting with NBFC representatives to understand their challenges but outcomes are unclear

Covid19 Tech Impact

Latest updates & innovations, in-depth resources, live webinars and guides to help businesses navigate through the impact of the COVID19 pandemic on India's economy.

“SME lending has totally stopped. Consumer lending is happening but only to the premium segment, which traditionally does not have such high demand as the middle and lower-income where the need is now even more acute.” — Bala Parthasarathy, cofounder and CEO, MoneyTap.

The sentiments shared by Parthasarathy with Inc42 clearly depicts the bleak scenario the lending industry in India is facing at the moment. But the situation is even worse for the NBFC segment in the digital domain. Being the niche sector amid the web of traditional large NBFCs and banks, the sector has been dependent on other NBFCs and banks for its credit supply.

Banks who support digital lending platforms in times of fund need are slowly decreasing their credit line. This has resulted in a liquidity crunch across the digital NBFC sector with lenders revisiting their customer profiles and giving loans to only those with good credit history. They are also revising the credit limits of individual borrowers.

Overall, since the ILF&S crisis in September 2018, the NBFC segment has attracted negative sentiment from the investor side. The sector had to face a slowdown in disbursements, reduced capital market borrowing, and more. While it has been gradually recovering from the crisis, the Covid-19 situation turned the screws in again, bringing newer challenges across the asset side and stressing NBFCs even further.

“Given the clampdown on economic activity in the past few weeks, the industry is most likely to see a spike in NPAs. The credit cost ratios are also going to increase which will impact the whole lending ecosystem wherein the lenders will become more risk-averse. The industry’s revenue streams are going to get impacted with reduced transactions, repayments, etc,” said Neel Juriasingani, CEO and cofounder, Datacultr.

Measures Taken By RBI So Far

Earlier, the RBI announced a few measures to provide some relief to the sector in terms of maintaining the required liquidity to continue lending operations. This primarily included:

Relaxation On NPA Classification

As stated by RBI, in respect of all accounts for which lending institutions decide to grant moratorium or deferment, and which were standard as on March 1, 2020, the 90-day NPA norm shall exclude the moratorium period, i.e., there would an asset classification standstill for all such accounts from March 1, 2020, to May 31, 2020.

“This is a good move and will prevent a sudden surge in NPA from 9% to 14-15% levels for the industry,” said Ram Iyer, founder and CEO, Vayana Network.

Targeted Long Term Repo Operations 2.0 (TLTRO-2)

RBI announced that it would conduct TLTRO 2.0 at the policy repo rate for tenors up to three years for a total amount of up to INR 50,000 Cr, to begin with, in tranches of appropriate sizes. The funds availed under TLTRO 2.0 shall be deployed in investment-grade bonds, commercial paper (CPs) and non-convertible debentures (NCDs) of NBFCs.

The first auction under TLTRO 2.0 was conducted on April 23, 2020, which reportedly did not receive a good response as only bids worth INR 12, 850 Cr were received.

Funding Through SIDBI, NABARD And NHB

The tenure of these loans will be 90 days. “We were provided with a special liquidity window of INR 15,000 Cr by the Reserve Bank of India (RBI) to enable MSMEs to tide over their liquidity crunch,” said Mohammad Mustafa, IAS, Chairman and Managing Director of SIDBI in a media statement.

Who Are The Eligible NBFCs?

- Should be registered with RBI as Investment and Credit Company (ICC)

- Should have been in business for at least 3 years

- Should have a minimum net owned funds of INR 20 Cr

- Should have an asset size of at least INR 50 Cr

- Credit rating of the NBFCs should be a minimum of ‘BBB-‘ or equivalent as on March 31, 2020

- Should have complied to applicable regulatory requirements

- The promoter/equity should not be in any RBI blacklist or defaulters list

- The Capital Adequacy Ratio (CAR) should always be above RBI requirements during the last 24 months

However, these moves by RBI have not been able to woo the NBFC sector. “There has been a fair amount of ambiguity on the effectiveness of the RBI measures and its dissemination to the needy small businesses/customer segments. While there is a lot of liquidity provided, it is not flowing through, at the moment and there isn’t enough visibility for the future too,” said Manish Lunia, cofounder, Flexi Loans.

Digital NBFCs: The Expectation From RBI

The Reserve Bank of India on Monday (May 4) met the representatives of leading NBFCs to understand the challenges faced due to Covid-19 pandemic. According to a CNBC report, the community put forward many demands. This primarily includes:

- Moratorium on loans for NBFCs: NBFCs to be given moratorium on their liabilities as well to ensure financial and liquidity stability to the sector.

- Allowing a one-time restructuring window: Till March 2021 for amending the loan repayment schedules and/or extending loan tenures or restructuring the EMIs, without affecting the asset classification

- Tackling funding issues: To consider providing funds to a refinance mechanism through SIDBI, NABARD and/or their associate institutions which can provide long term loans to NBFCs for their on-lending operations. consider allocating the unsubscribed part of TLTRO 2.0 to these institutions as well.

- Provisioning requirement on moratorium loans: The RBI notification dated April 17, 2020 requires a provision of up to 10% in respect of all loans which are at least 1 day past due and where a moratorium has been granted. NBFCs request to permit provisioning to be made where moratorium has been given only on loans that are 30 or more days past due.

Inc42 talked to a number of digital NBFCs on these issues. Most believe there are a few other points that the RBI should consider.

Deferment Of Accumulated Interest

In the case of working capital, limits like overdrafts/cash credits moratorium on payment of interest is allowed till June. But the RBI wants the accumulated accrued interest of three months to be paid ‘immediately’ on the conclusion of the deferment period. This again will cause immense agony to the borrowers as their already strained cash flows will in no way help them to meet this huge demand all of a sudden. The deferment, therefore, becomes deadly because of this rider, said Vayana Network’s Iyer.

TLTRO 2.0 for More Investment Grade Entities

Many lending startups (NBFCs) are unrated or rated below investment grade which are largely dependent on a set of large NBFCs or some Small Finance Banks. It will be critical to see how the money from TLTRO 2.0 flows into these unrated/below investment grade NBFCs borrowing from these financiers.

“For TLTROs to be really successful it is important that benefit is widespread and not end up being concentrated to few large NBFCs/MFIs,” said Ashish Kohli, Managing Director and CEO, Kreditech India.

Also, the NBFCs are looking for measures to allow the use of e-KYC to enable loan availability through digital channels and ease the digital flow for lending and repayments dramatically.

NBFCs: The Strong End

According to a recent report by CARE Ratings, there has been an improvement in capital adequacy ratio (CAR) and leverage position of both NBFCs and HFCs since September 2018. “However, the loan book growth was diluted by most companies as the focus has been on balance sheet strengthening rather than profitability or growth,” the report added.

The analysts believe that NBFCs have enough on-balance sheet liquidity to tackle the 3-month moratorium period (of which March 2020 collections seem to have been close to normal). The current situation is not as bleak for larger NBFCs with backing from corporate groups and the Indian government.

For instance, U GRO Capital, a BSE-listed technology-enabled small business lending platform managed to redeem NCDs before the maturity date while complying with RBI COVId-19 moratorium policy.

“We have created a granular and diversified liability line which includes multiple terms loans from PSU and private sector banks. We have also actively securitised portfolios. All these have enabled us in facilitating the early redemption of the NCDs in a pretty challenging economic environment,” said Shachindra Nath, executive chairman and managing director, U GRO Capital.

Fighting Challenges The Digital Way

Analysts believe that the key challenge will arrive post the moratorium period, assuming the country-wide lockdowns end by May 2020. Once lockdown opens, it will take time for collection efficiencies to normalise.

Also, NBFCs and digital lenders would have to factor in sections where lockdown still continues. With RBI looking to extend moratorium further for 3 months, it will also become a liquidity constraint for the entire lending segment.

To be noted, NBFCs dependent on physical collections have been impacted more than those operating digitally on a partial or full basis.

“For many of us, the collection ratios are fairly good where customers are themselves not choosing the moratoriums. Even where moratoriums are chosen, customers want the lockdown to open to pay the EMIs vs. waiting till June,” FlexiLoans’ Lunia.

Another digital NBFC and lending player True Balance continues to offer loans in small ticket sizes.

“Lending in March 2020 was ~INR 23 crore nationwide. The ticket sizes of these loans range between INR 5,000 – INR 7,000, and the firm continues to disburse more than 40,000 loans daily, which are majorly used for running households,” claimed Charlie Lee, Founder and CEO, True Balance

With RBI looking to further extend the moratorium for another three months and lockdowns seemingly not ending anytime soon, the situation is likely to worsen for the lending industry. Thus, this is the time to use data about customer’s transactions, repayment potential and other psychometric and demographic data to make smart decisions about potentially deserving customers in the future. However, the momentum will take time and capital, the latter of which is in short supply in the market.