SUMMARY

Who is supposed to pay the Account aggregators for their services? The AAs, in today’s format, are struggling to make peace in terms of practicability, applicability and its revenue model

Like ecommerce and UPI payments startups, AAs will be high on data, low on profit margin; a challenge for their survivability

Besides the RBI, the AAs will deal with a host of data transactions pertaining to areas of other regulatory bodies such as SEBI, IRDAI, PFRDA and FSDC

India's Digital Lending Reset

India’s digital lending sector is currently in a reset mode as the contracting GDP, moratorium, & Covid-19 has forced companies to adopt digital, review credit models & more. This playbook takes a deep dive into the challenges and new pathways adopted by digital lending startups for survival and scale!

The pandemic may have forced lenders to go digital for B2B loans, eligibility criteria and risk, and approval process, but that does not guarantee that more loans will be processed because there’s a glaring hole in the middle of the Indian B2B credit market — lack of data.

While things like video KYC have helped digital NBFCs and lending tech startups to authenticate potential customers, this is still not good enough to get loans approved. For business loans, the criteria vary from business to business and sector to sector. So how can digital lenders hope to keep up with all these various criteria and will businesses seeking loans even have supporting documents?

Envisioning a paperless future, the account aggregator (AA) system promises to bring low-cost validated data to every lender in the market — at once solving the data problem. If in July 2019, Nandan Nilekani formally introduced the concept of account aggregators, in July this year, Nilekani has further introduced OCEN (Open Credit Enablement Network) developed by iSPIRT Foundation which would work as a common language between LSPs (Loan Service Providers) and lenders.

At the Global Fintech Festival, Nilekani said,

“Lenders focus on blue-collared workforce, want to solve cost and data asymmetry. Cost is solved by digitisation and asymmetry is solved by the Account Aggregator model. Now, credit protocol (OCEN) will democratise the process for millions of small businesses. For our economy to revive we need to fund small businesses.”

As the AAs are currently under testing period and now expected to go live in a few months, lending startups while agreeing with the immense potential that AAs may unleash down the line, have also raised a slew of issues in terms of account aggregators’ applicability and practicability.

Account Aggregators Take Baby Steps

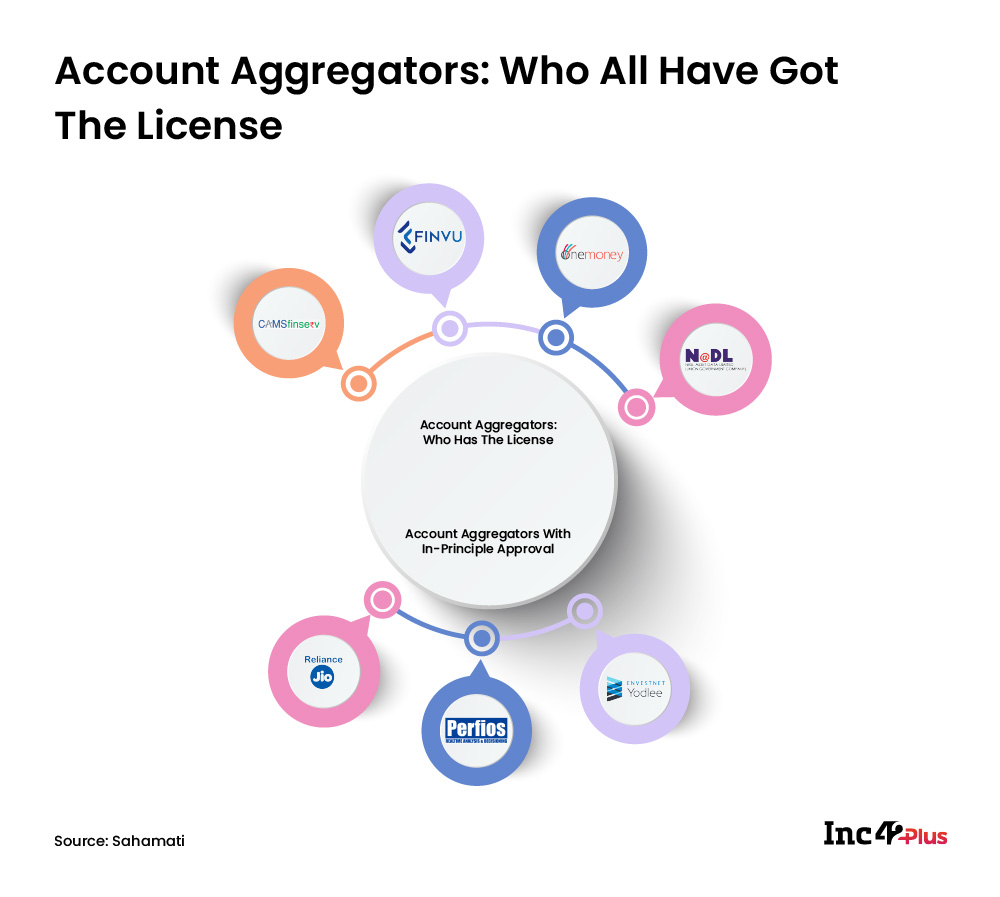

It has been over six months since the RBI extended its in-principle approval and operating licenses to a slew of NBFCs for account aggregation i.e streamlining and structuring of data. The account aggregators which have been in the testing phase since January this year were supposed to be completely operational by June 2020, but have now been pushed to December, 2020.

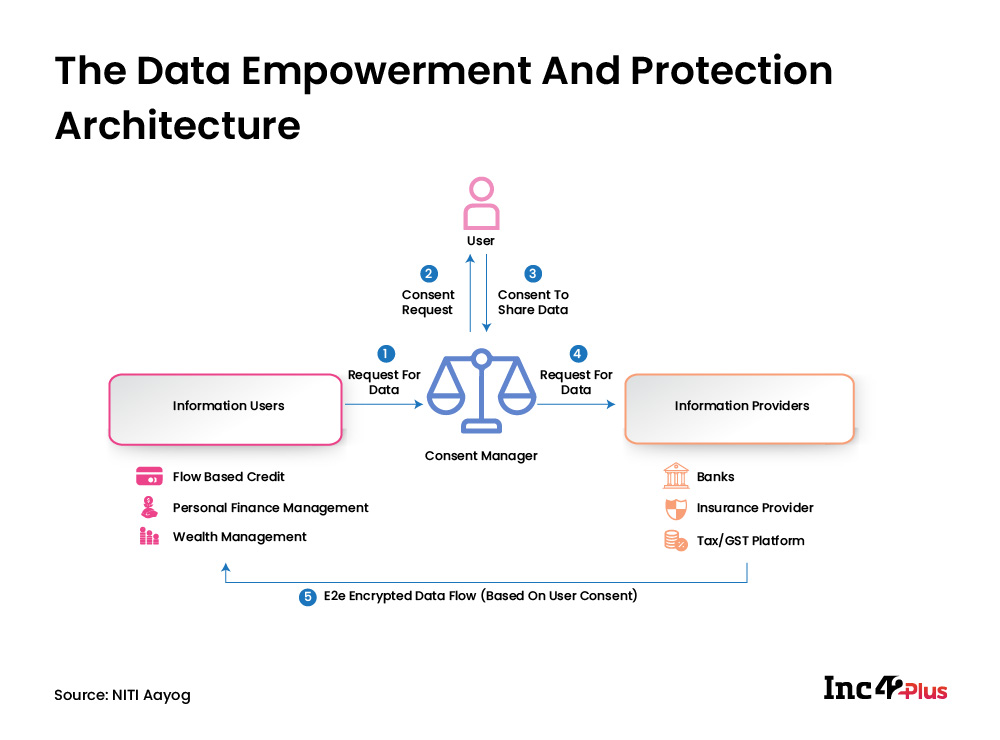

Behind the account aggregator system is the Data Empowerment and Protection Architecture (DEPA) which is also the same data consent mechanism to be adopted in India’s healthcare system soon. At a time when India has hardly any standard data privacy norms in place and the upcoming Personal Data Protection bill too is languishing in the parliament. Even so, in its present format, the PDP bill does not ensure data protection, as Justice Srikrishna, the chairman of the bill’s drafting committee, said.

Arguably, DEPA is expected to improve the existing data security practices for financial information users and financial information providers. Bringing transparency in terms of digital data footprints and consent mechanism, DEPA seeks to connect the three key building blocks — regulatory standards, digital infrastructure and public and private entities.

However, most of the lending startups and NBFCs stated that the DEPA and account aggregator seem promising on paper but have implementation issues. Moreover, it will take years to have clarity in terms of its adoption and implementation.

Mithun Sundar, CEO of Lendingkart Finance, agreed that DEPA will reduce the frictional issues for lending companies in terms of data collection and its validation. It is a win-win for all the stakeholders but will take at least 12-24 months to evolve.

Speaking to Inc42, BG Mahesh, cofounder of Sahamati, a collective of account aggregator ecosystem, stated that one must understand and agree to the fact that the account aggregator ecosystem, besides being a massive project, is in its stage one.

“We have had a great start with the largest banks who have embraced the Account Aggregator framework. We are confident of seeing a large adoption of AA over the next few years.For instance, UPI payments which has now crossed 1.5 Bn transactions a month didn’t happen in a few months; it took over a year before all the major banks joined the UPI platform,” Mahesh said.

There is also a reason behind starting this with the banking companies and not with insurance or other companies. It’s because banking has got the highest penetration among all, added Mahesh.

Axis Bank, Bajaj Finserv, DMI Finance, Federal Bank, HDFC Bank, ICICI Bank, IDFC FIRST Bank, Indusind Bank, SBI and the four account aggregators with operating licenses (CAMS, FinVu, NADL, Onemoney) are in the process of going live on the AA Ecosystem.

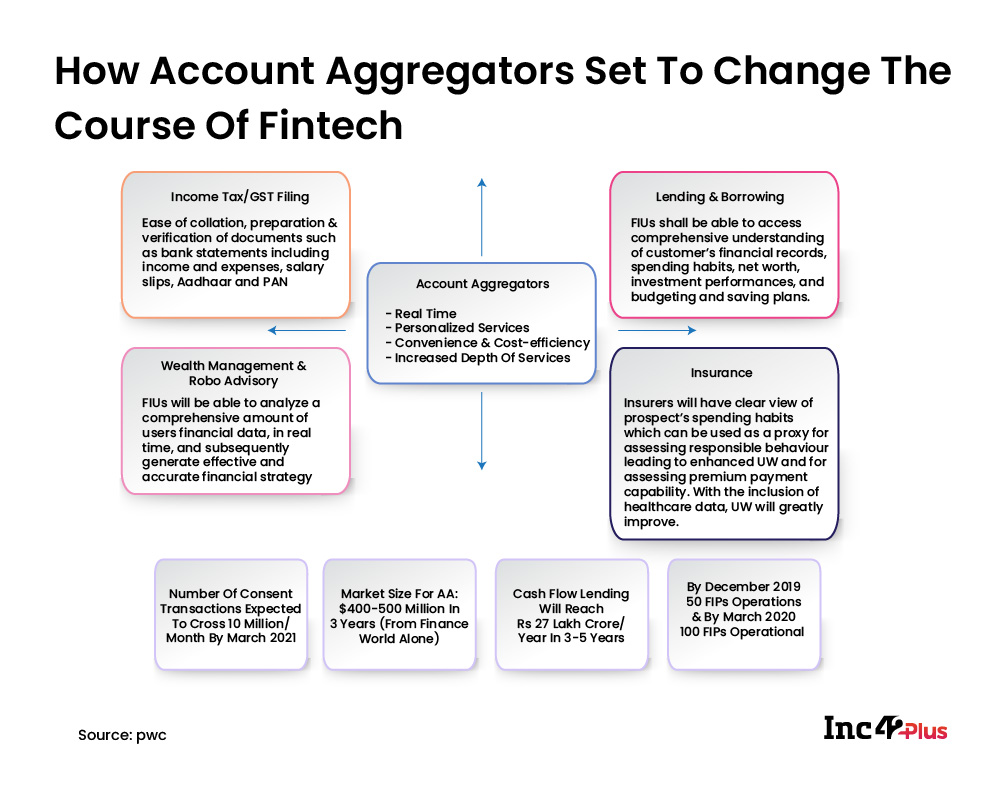

Sahamati, in its blog, has claimed that AAs could help 1 Bn underserved Indians for whom there is no credit bureau file and 58 Mn MSMEs get access to formal credit.

Account aggregators are not only expected to bring a real-time consent mechanism for quick and authenticated access to financial data but can be used to build customised fintech products for niche segments, monitor loan defaults and therefore lending risk in particular sectors, create better customer service benchmarks based on data and more.

The public think-tank NITI Aayog recently published a discussion paper on account aggregators which suggested that AA in conjunction with other platforms like the public credit registry and open credit enablement network (OCEN) allow lending companies to diversify their credit products — through sachet-sized for individuals and regular flow-based lending to MSMEs. These new data-led systems will allow for more sophisticated and cost-effective credit scoring models as well.

The iSPIRT Foundation, responsible for developing the tech stack and the APIs for AA, expects account aggregators to become a new class of companies that would help create new data-oriented markets and opportunities for entrepreneurs.

How Practical Is Account Aggregator At Present?

The idea behind account aggregators is to not only to bridge the gap among information seekers, providers and beneficiaries/consumers but also to customise the loan products with the help of OCEN. Accountant aggregators act as middlemen to lenders based on the consent of the borrower. This is the concept to streamline the data access, to be regulated by RBI. But it is still far away from implementation.

Madhusudan Ekambaram, CEO of personal loan platform KreditBee said that account aggregators have been a very wonderful development but there are several issues pertaining to its real impact.

“There are a lot of questions on the model regarding its practicability. The entire revenue model around such NBFCs is not very clear. Secondly, the practical applicability in the market is also not very clear. Few licenses have already been issued by RBI, but none of these companies has been able to figure out a clear model. They are struggling with access to users’ information as well,” said Madhusudan E.

Seconding Ekambaram, multiple founders told us that account aggregators have been facing issues pertaining to accessing the consumer and MSME data. Also, in the case of dispute, there are chances of it getting delayed. Currently, the borrowers while applying for loans give lenders, direct access to their banking which then automatically verifies the borrowers’ account details and data.

Sahamati’s Mahesh however averred that account aggregators democratise the access to data. “We have been actively engaging with every stakeholder and we respond to every query we receive. It must be noted that the RBI in its master directions has already provided clarity on all issues for the Account Aggregator Ecosystem. Regarding customer grievance redressal, every AA will have a policy for handling/ disposal of customer grievances/ complaints. It shall have a dedicated set-up to address customer grievances/ complaints,” Mahesh added.

There Is No Consensus Over Who Will Bear The Cost

The practicability and applicability are not only issues. Saurabh Jhalaria, the CEO of SME loans, InCred, said, “The account aggregators will have to be more nimble in terms of costs. So if let’s say for every loan, if the account aggregators are charging 3% that may not be a viable proposition for both lenders and customers. So, the account aggregators will have to work with thin margins.”

In its latest discussion paper, NITI Aayog has simply initiated the discussion by saying consent managers can facilitate data exchange by charging a nominal fee. However, since most individuals are accustomed to free services, account aggregators could subsidise or relinquish the service fee charged to the data principals by charging the data users (much like a subscription model).

Information providers could also go charge a service fee in the future, but in the financial sector, they have agreed to provide data without a charge for the time being. Finally, a competitive ecosystem of AAs in each sector could keep prices manageable but cover costs to ensure profits, the NITI Aayog had stated.

The revenue model of AAs seems to have a similar deadlock that zero merchant discount rate (MDR) has created for payments companies that rely largely on UPI — with transactions growing exponentially, but revenue being next to nothing.

Do AAs Really Resolve The ‘Bharat’ Issues

AAs intend to help a billion Indian and MSMEs in getting customized loans at fingers tap by helping bring multiple FIPs and FIUs on a single platform through OCEN. However, it must be noted that a majority of consumers that belong to Bharat category or India 4 and India 5 categories as MoneyonClick founder Vishal Chopra calls it don’t have much digital trace or data to collect.

Account Aggregators would streamline the existing data, however, it will take decades before India 4 and India 5 (families which have a cumulative monthly income of 0- INR 50K) to have enough digital data in order to make use of OCEN model for the faster and better loan offers. For instance, in the case of agriculture, farmers selling their produce in the market has not been quantifiable digitally. Gross transactions or cash flow cannot be the criteria for the unsecured loans that are being offered to them. The quantification of produce, their current and future market price also needs validation, which is not possible without physical intervention.

Also, much of the digital data has not been updated as often as it should be. For instance, a significant chunk of Aadhaar data has not been correctly linked with corresponding addresses and mobile numbers. Consumers have not updated details either in their bank accounts or anywhere else. In a significant number of cases, even the borrowers’ names/father’s names don’t match with their corresponding documents. Account aggregators simply provide a data-sharing model and hence lack to have a space for such correction which would again be manually done, said multiple founders.

On having the scope of data correction or updating them in the account aggregator architecture, Mahesh further clarified that the AAs simply help in handshaking the FIPs and FIUs for data sharing. Account Aggregator shall not support transactions by customers, the AA framework is for consented data sharing only.

Some lenders also suspect the quality of the digital data and question the reliability of income tax returns, transactions which have not been reliable enough to be the basis to lend money. Some of the lending startups agreed to the argument that neither the income tax returns nor the payment transaction records as it mostly happen in the form of cash reflect the true loan potential of a rural entrepreneur such as kirana store owner or a farmer. In most of the Bharat related cases, you have to be ready for physical verifications and assessments. And, if you’re, AAs won’t make much sense for you.

Lack of Data Protection Authority

Currently, the handful of AAs in India have adopted the data consent mechanism that the Personal Data Protection Bill has proposed in its draft. As the Bill is still on the table of the Joint Parliamentary Committee and thus has not been cleared by the parliament, many of the provisions of the bill do not exist as of now. Establishing a Data Protection Authority is one of them.

The RBI has been mandated to extend licenses to the account aggregators. In its April 6, 2018 notification, the RBI had directed all the system providers to ensure that the entire data relating to payment systems are stored in a system only in India.

“This data should include the full end-to-end transaction details/information collected/carried/processed as part of the message/payment instruction. For the foreign leg of the transaction, if any, the data can also be stored in a foreign country, if required.”

However, these account aggregators will be dealing with the data that are regulated by other regulatory authorities like SEBI, IRDAI, PFRDA and FSDC. In the case of any data-related dispute, there is no single authority like the Data Protection Authority which would govern or monitor the data-flow.

The Central Data Protection Authority and its State counterparts till date remain on paper and this is where despite promising better efficiency, transparency and consent mechanism, not all stakeholders are equally convinced about the idea of AAs.

Is India Prepared For Next-Gen Fintech?

In spite of the initial hiccups, Data Empowerment and Protection Architecture (DEPA) is bound to bring a paradigm shift in India’s BFSI sector at large, experts believe.

DEPA is an attempt to replicate the UK’s open banking APIs like architecture which now has over 2 Mn users for India’s entire fintech needs. Europe too has a similar open banking infrastructure with a growing number of users.

In the case of India, it is however argued that AAs are not a matter of choice but probably would soon be an essential way of consent mechanism given its huge data transaction needs.

Gaurav Aggrawal, director and business head, PaisaBazaar told Inc42, “Account aggregators are going to democratise the access of transactional data, whether it is the consumer side or the business side. However, since it involves a lot of participants whether it is people who are going to be using that data or the ones who would provide that data, I think the process will take some time to become reality.”

Rarely does it happen that a policy change empowers both consumers as well as the businesses. Abhijit Ghosh, CEO of U GRO Capital, said, “DEPA redefines the consent mechanism by empowering them on consensus. The consumers can now decide for what period of time or how many times, the lenders can access their GST file or other documents that the consumers want to share. So, there’s a very, very fundamental reason that I feel that this will change the paradigm.”

Being a multi-party ecosystem, awareness, therefore, will be the key parameter in the adoption and acceptance of account aggregators from both businesses and consumers. Lenders and fintech startups need to learn the new way of getting authenticated data.

Is the account aggregator system ahead of its time for the Indian market, as many feel given that the digital penetration is simply not there yet for the data streamlining and structuring and the problems with the quality of data?